What’s Really Going On With Social Security?

By Katelyn Pollard, CFP®

Recent headlines have raised concerns for many working Americans, suggesting that Social Security may not be around by the time they retire. Let’s take a closer look to understand what’s really going on, because the reality is more nuanced, and far less alarming, than the headlines imply.

How Social Security is Funded–and Why That Matters

Social Security is primarily funded through payroll taxes collected under the Federal Insurance Contributions Act (FICA). Both employees and employers contribute a portion of wages, and self-employed individuals pay the equivalent amount through self-employment taxes. This steady stream of payroll taxes is the main source of funding for current benefits.

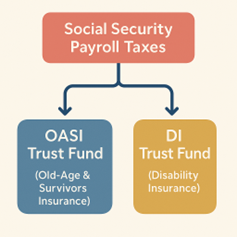

The funds collected go into two trust funds: the Old-Age and Survivors Insurance (OASI) Trust Fund and the Disability Insurance (DI) Trust Fund. These trust funds are managed by the U.S. Treasury and invested in special-issue Treasury bonds backed by the full faith and credit of the U.S. government. This means the funds are held securely and generate interest, helping to support Social Security payments.

The Reality Behind the Headlines

Social Security is not going bankrupt, but there is some truth to the headlines. Projections indicate that by 2035, the trust fund reserves, or the program’s accumulated savings, could be depleted if no changes are made. After that, Social Security would rely solely on payroll tax revenue, which is expected to cover about 83% of scheduled benefits.

This projected 17% funding shortfall does not mean benefits will disappear. Rather, it indicates that benefit reductions may be necessary if lawmakers do not take action, and historically, they have. The last major Social Security reform occurred in 1983, when Congress implemented a combination of tax increases and benefit changes to help secure the program’s future. Today, potential solutions include raising the payroll tax cap, modestly increasing the retirement age, or reducing benefits for higher-income earners.

Looking Ahead with Confidence

While the headlines can feel unsettling, the core of Social Security remains strong. With careful planning and realistic expectations, Social Security can continue to be a reliable and important part of your financial plan.

We’re here to help you navigate these concerns and provide a thoughtful second opinion whenever you need one. Understanding the potential changes, and keeping a clear, steady perspective, can help you stay confident about your retirement future.

JGP Wealth Management is a registered investment adviser. This brochure is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by JGP Wealth Management unless a client service agreement is in place.

This commentary reflects the personal opinions, viewpoints and analyses of the JGP Wealth Management employees providing such comments, and should not be regarded as a description of advisory services provided by JGP Wealth Management or performance returns of any JGP Wealth Management client. The views reflected in the commentary are subject to change at any time without notice. Nothing in this commentary constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. JGP Wealth Management manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.